The global in vitro diagnostics (IVD) industry plays a fundamental role in modern healthcare by enabling the detection, monitoring, and management of diseases through laboratory analysis of biological samples such as blood, urine, and tissue. Diagnostic testing supports clinical decision-making, assists physicians in identifying diseases at early stages, and helps guide personalized treatment strategies.

In recent years, the importance of diagnostic technologies has increased significantly as healthcare systems worldwide focus on preventive medicine and early disease detection. Advanced diagnostic platforms allow healthcare providers to obtain accurate and timely clinical insights, improving patient outcomes and supporting data-driven healthcare delivery.

The integration of automated laboratory systems, digital health platforms, and molecular diagnostic technologies is transforming diagnostic workflows globally. These innovations improve testing efficiency, increase diagnostic accuracy, and enable faster delivery of patient care.

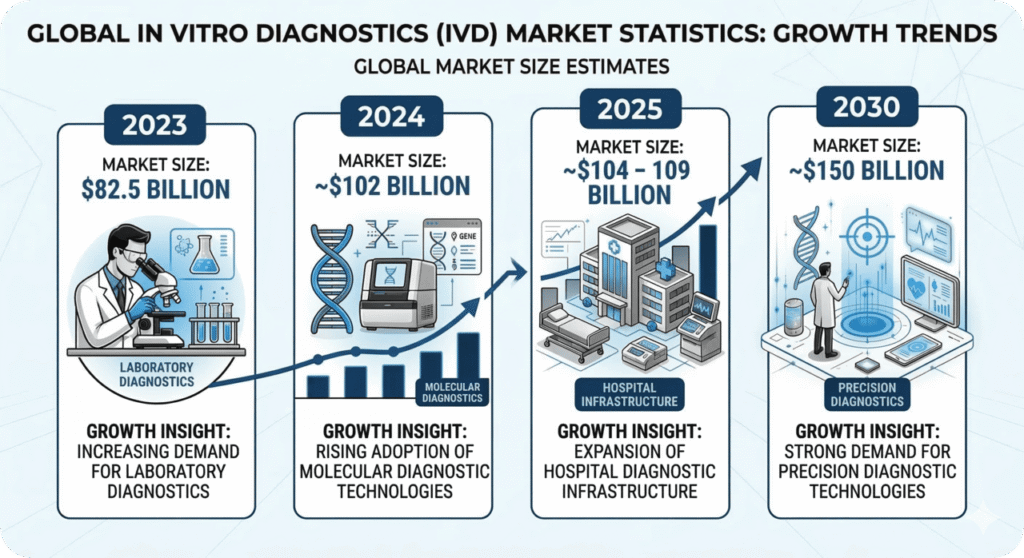

The global in vitro diagnostics market continues to demonstrate steady expansion as healthcare providers increasingly rely on advanced testing technologies for disease detection and monitoring. The market was valued at approximately USD 106.29 billion in 2025 and is projected to reach nearly USD 128.18 billion by 2033, registering a compound annual growth rate (CAGR) of approximately 2.40% during the forecast period.

Growing demand for rapid diagnostic solutions across hospitals, clinical laboratories, and home-care environments is expected to support continued market expansion. Additionally, increasing adoption of point-of-care diagnostics and decentralized testing technologies is improving accessibility to healthcare services worldwide.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

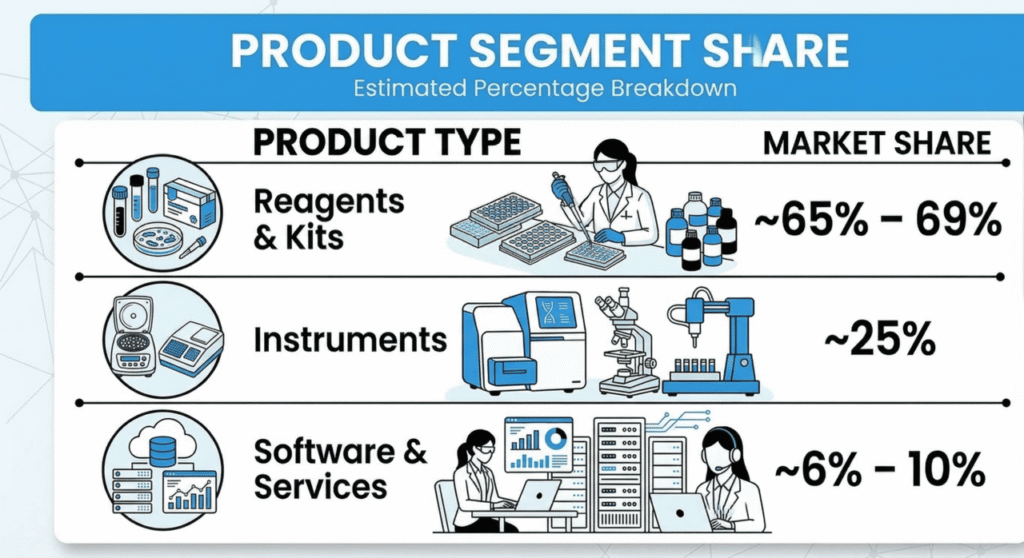

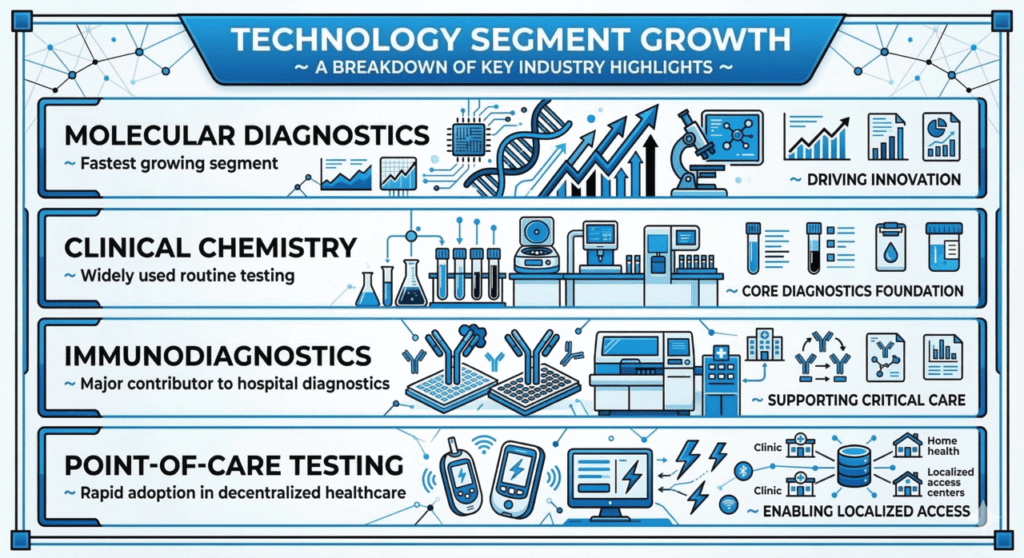

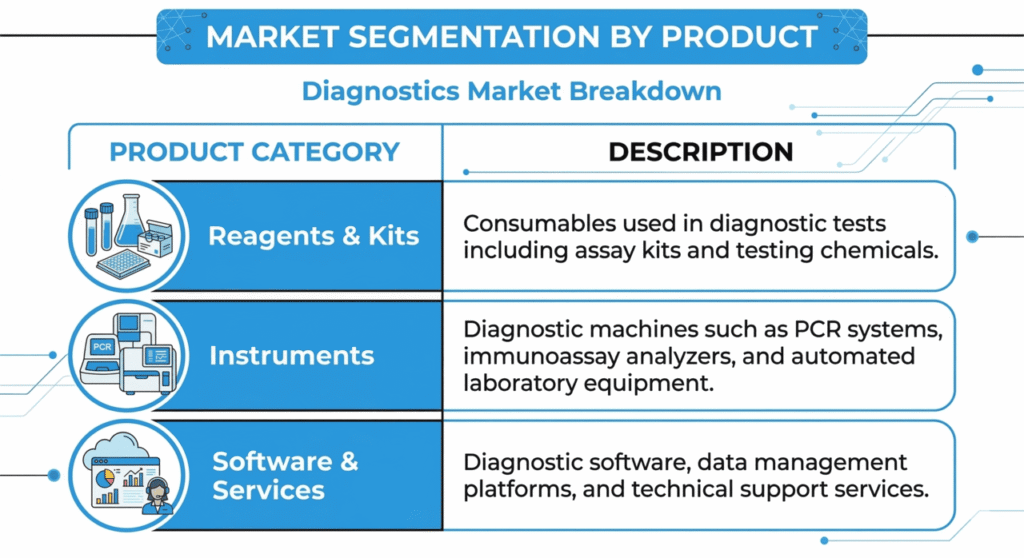

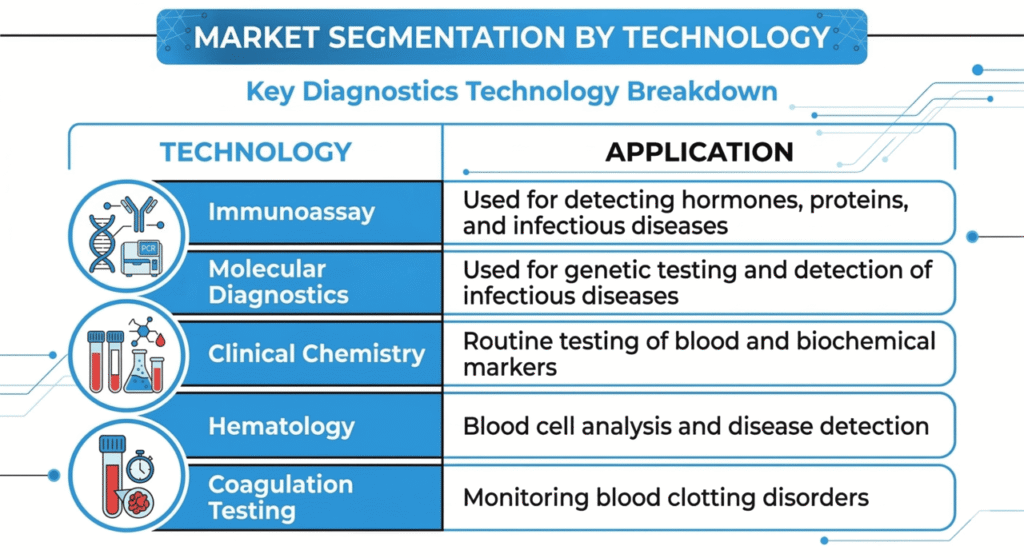

Several segments continue to dominate the global IVD market due to their widespread clinical applications. Reagents accounted for the largest share because they are essential consumables used in routine laboratory testing. Molecular diagnostics technologies also hold a significant portion of the market due to their high sensitivity and accuracy in disease detection.

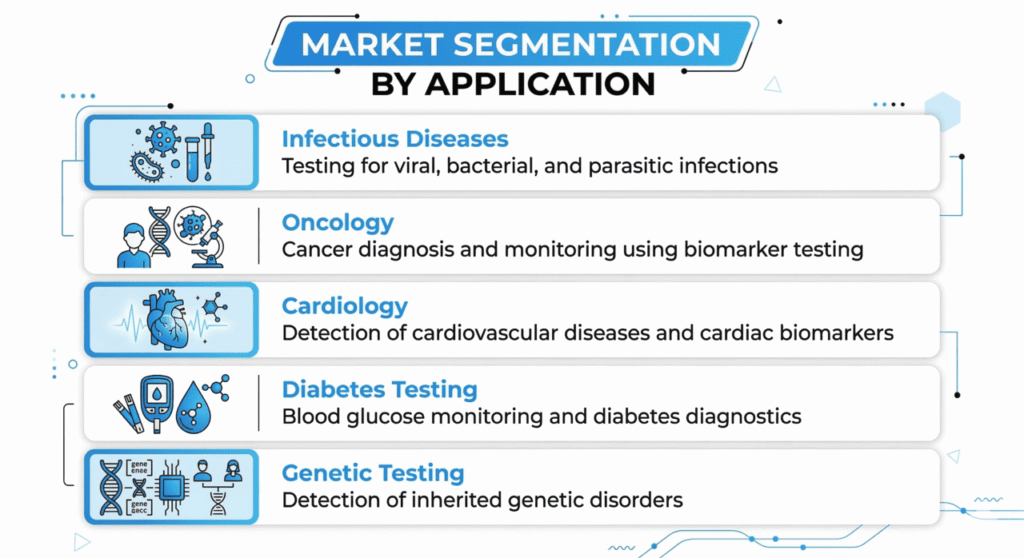

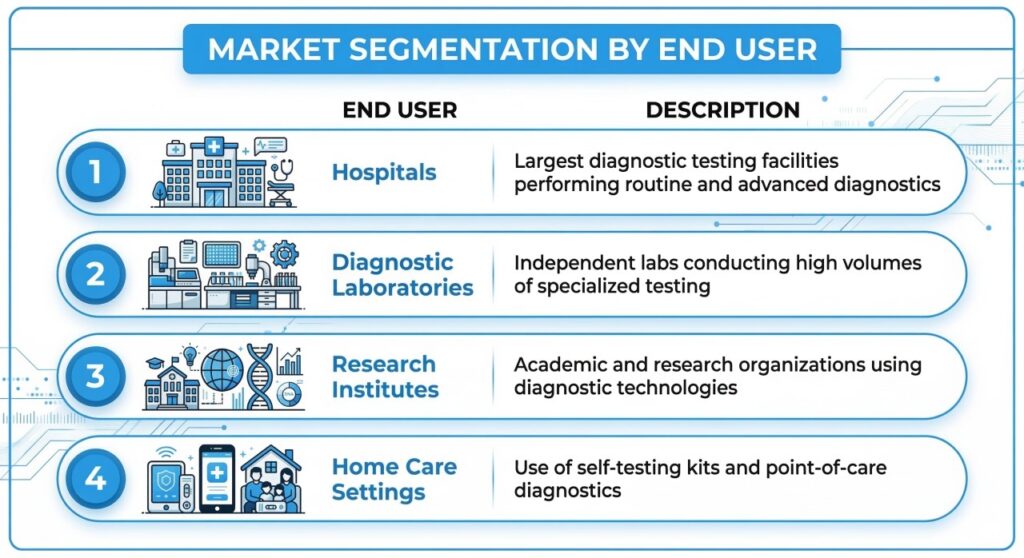

Infectious disease diagnostics represent the largest application segment globally, driven by the need for rapid detection and monitoring of viral and bacterial infections. Hospitals remain the primary end users due to the high volume of diagnostic procedures performed in clinical environments.

The rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, cancer, and respiratory illnesses is a major factor driving the demand for diagnostic testing. Early detection of these conditions allows healthcare providers to initiate treatment earlier and improve patient outcomes.

Technological innovation is another key driver shaping the IVD market. Advances in molecular diagnostics, next-generation sequencing, and automated laboratory platforms have significantly improved diagnostic precision and efficiency.

Technological innovation continues to transform the diagnostic testing landscape. Advances in microfluidics, nanotechnology, and instrument miniaturization are enabling the development of compact diagnostic devices capable of delivering rapid and reliable results.

Point-of-care diagnostic systems are becoming increasingly important as they allow tests to be performed near the patient and provide results within minutes. These technologies are particularly useful in emergency care, infectious disease detection, and rural healthcare settings.

Despite steady growth, certain challenges continue to affect market expansion. High costs associated with advanced diagnostic equipment and molecular testing platforms can limit adoption among smaller healthcare facilities.

Regulatory requirements also create barriers for manufacturers, as diagnostic products must undergo rigorous validation and approval processes before entering the market.

The growing adoption of personalized medicine presents major opportunities for the IVD market. Companion diagnostics are increasingly used to identify patients who will benefit from targeted therapies, particularly in oncology and genetic medicine.

Additionally, expanding healthcare infrastructure in developing economies is creating new demand for advanced diagnostic technologies.

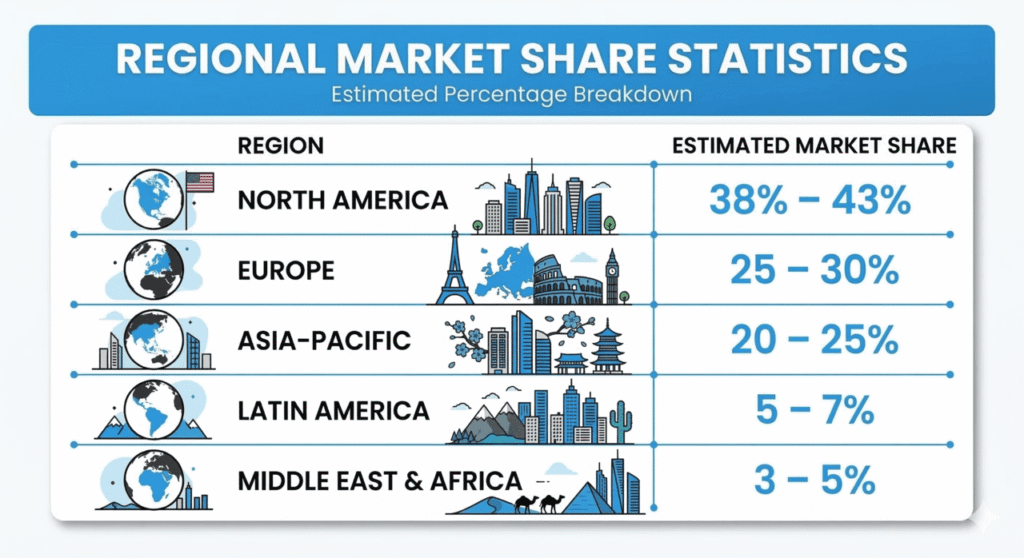

North America currently leads the global IVD market due to strong healthcare infrastructure, high healthcare spending, and the presence of leading diagnostic companies. Europe represents a mature market with strong regulatory frameworks and public healthcare systems.

The Asia-Pacific region is expected to witness the fastest growth due to increasing healthcare investments, growing population, and rising awareness of early disease detection.

In vitro diagnostics are medical tests performed on biological samples such as blood, urine, or tissue outside the human body to detect diseases, monitor health conditions, and guide treatment decisions.

The market is driven by increasing prevalence of chronic diseases, technological advancements in molecular diagnostics, expansion of healthcare infrastructure, and rising demand for rapid diagnostic testing.

North America currently holds the largest share of the market due to advanced healthcare infrastructure and strong investment in medical research.

Molecular diagnostics is among the fastest-growing segments because of its ability to detect diseases at early stages with high precision.

Reagents are used in routine laboratory testing and must be replenished frequently, making them the largest revenue-generating segment in the IVD market.