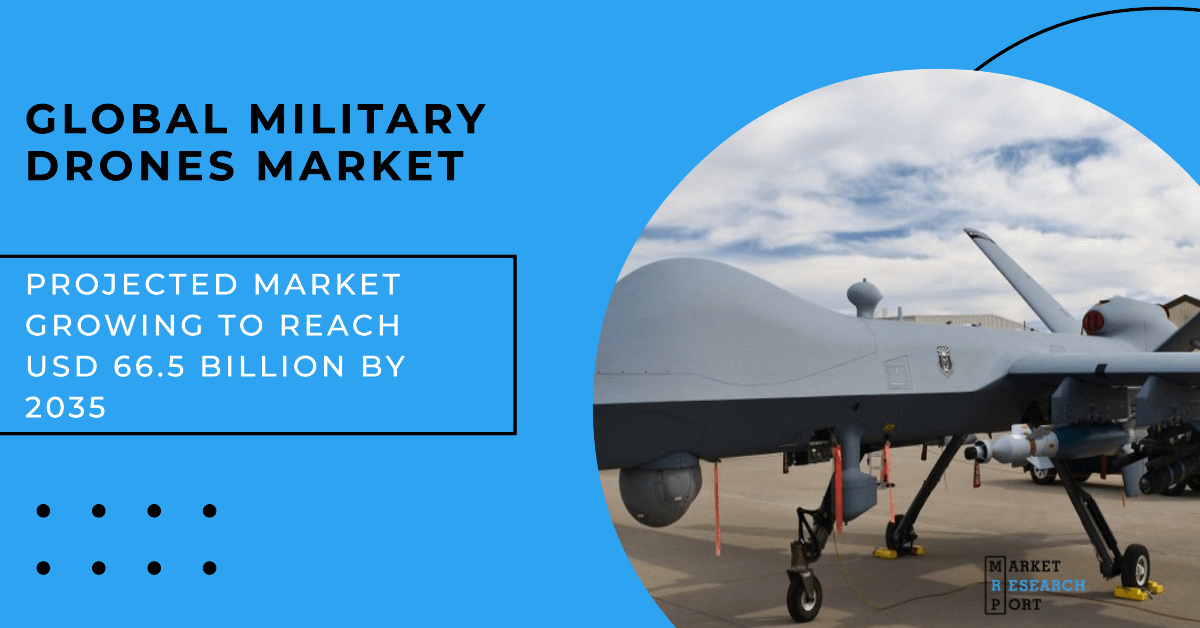

The global Military Drones Market was valued at USD 18.2 billion in 2025, reflecting the growing importance of unmanned systems in modern defense operations. Supported by rapid advancements in autonomous flight technologies, artificial intelligence, and increased defense modernization initiatives, the market is projected to expand to USD 20.7 billion in 2026, reach approximately USD 39.4 billion by 2031, and further surge to nearly USD 66.5 billion by 2035. This expansion represents a robust compound annual growth rate (CAGR) of 13.8% over the forecast period, according to Global Market Insights Inc.

Military drones have become a cornerstone of contemporary defense strategies across the globe. Their ability to execute intelligence, surveillance, and reconnaissance (ISR) missions, conduct precision strikes, and operate in hostile or inaccessible environments without risking human lives is significantly accelerating adoption across army, navy, and air force operations.

The growth of the Military Drones Market is strongly supported by increasing global defense spending and a strategic shift toward unmanned and autonomous combat systems. Defense agencies worldwide are prioritizing drone deployments to strengthen border surveillance, maritime patrol, electronic warfare, and real-time battlefield intelligence capabilities.

Rising geopolitical tensions and regional conflicts are further intensifying demand. For example, in August 2023, the U.S. Department of Defense expanded its focus on unmanned aerial systems through the Replicator initiative, aimed at accelerating the large-scale deployment of military drones for ISR and combat missions.

NATO member countries are also increasing investments in High-Altitude Long-Endurance (HALE) and Medium-Altitude Long-Endurance (MALE) drone platforms to ensure persistent surveillance and operational interoperability. Meanwhile, nations across Asia-Pacific and the Middle East are strengthening indigenous manufacturing capabilities and imports of military drones to address border security, maritime threats, and asymmetric warfare challenges.

The Military Drones Market experienced steady growth between 2022 and 2024, expanding from USD 12.5 billion in 2022 to USD 16.1 billion in 2024. This growth was primarily driven by increasing investments in ISR platforms and the rising need for real-time situational awareness on the battlefield.

Large-scale procurement programs across the United States and Europe have contributed to stable production pipelines and long-term order backlogs. Defense forces are increasingly investing in collaborative combat aircraft, long-endurance surveillance drones, and interoperable MALE platforms, highlighting a long-term transition toward unmanned force structures.

In November 2025, Rift secured approximately USD 5.2 million in funding to develop real-time aerial intelligence solutions, aiming to scale autonomous military drone operations managed from centralized remote command centers in France.

| Metric | Details |

|---|---|

| Base Year | 2025 |

| Market Size (2025) | USD 18.2 Billion |

| Market Size (2026) | USD 20.7 Billion |

| Forecast Period | 2026–2035 |

| Compound Annual Growth Rate | 13.8% |

| Projected Market Size (2035) | USD 66.5 Billion |

The Military Drones Market is moderately consolidated, with leading manufacturers accounting for approximately 31% of global revenue in 2025. Market leaders continue to strengthen their positions through technological innovation, platform upgrades, and long-term defense partnerships.

Northrop Grumman dominates the HALE segment, while IAI and General Atomics are recognized for combat-proven MALE and armed drone platforms. Thales and Lockheed Martin differentiate through advanced sensor integration, secure communication systems, stealth capabilities, and collaborative combat aircraft development.

North America remains the largest regional market, supported by substantial defense budgets, advanced manufacturing capabilities, and extensive deployment of military drones for border security and maritime surveillance.

Europe continues to witness steady growth due to collaborative ISR programs, rising defense investments, and initiatives to enhance domestic military drone production, with Germany playing a leading role.

Asia-Pacific is expected to register the fastest growth during the forecast period, driven by geopolitical tensions, border disputes, and rapid expansion of indigenous drone manufacturing in countries such as China and India.

Brazil leads the regional market, supported by increasing demand for border monitoring and long-endurance maritime surveillance operations.

Countries such as Saudi Arabia are increasing investments in military drones as part of comprehensive force modernization programs, focusing on airspace security and operations in extreme environmental conditions.

The Military Drones Market was valued at USD 18.2 billion in 2025.

The market is projected to grow at a CAGR of 13.8% from 2026 to 2035.

Rising defense spending, geopolitical tensions, and demand for ISR capabilities are key drivers.

Key applications include ISR, border surveillance, maritime patrol, and precision strike missions.

Fixed-wing, rotary-wing, and hybrid military drones are widely used.

They provide long-endurance surveillance and strategic intelligence capabilities.

Cybersecurity risks, electronic warfare threats, and strict export regulations.

North America leads, while Asia-Pacific shows the fastest growth.

Major players include Northrop Grumman, IAI, General Atomics, Thales, and Lockheed Martin.

The market is set for strong growth driven by AI, autonomy, and defense modernization.